Medicaid Planning: Miller Trust (8 Pages)

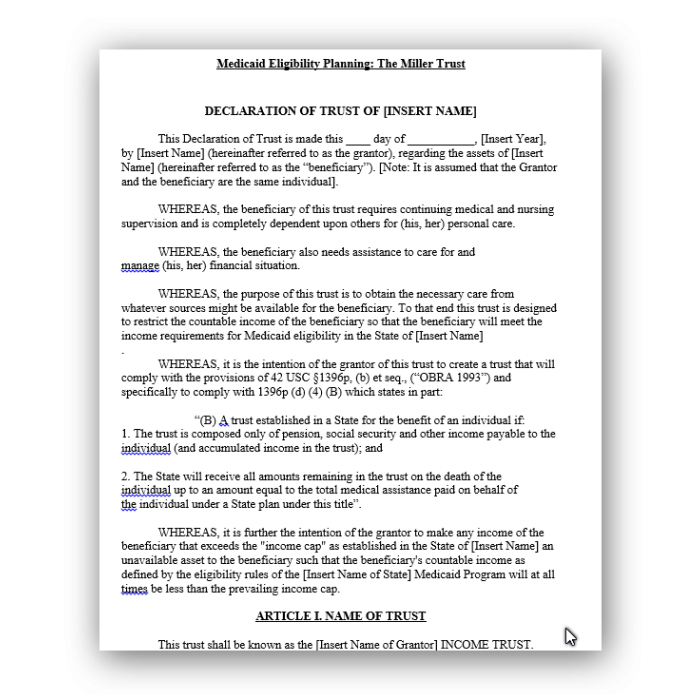

This is a Form of a “Miller Trust”, sometimes referred to as a “Qualified Income Trust”. The Trust takes its name from the case of Miller v. Ibarra, 746 F. Supp. 19 (D. Colo. 1990), and is specifically sanctioned by 42 U.S.C. § 1396p(d)(4)(B). The Trust may be used when the countable resources of a Medicaid applicant may be sufficiently low for Medicaid qualification, but the applicant’s monthly income is too high for those states that look to an income limit as a basis for Medicaid qualification. However, the available income is not enough to pay the cost of long-term care in a skilled nursing facility. This Trust is designed to address this problem by bridging the gap between the income cap for eligibility and the actual cost of nursing home care. The Miller trust is significant in those states which impose an income cap on Medicaid long-term care eligibility.

This is a Form of a “Miller Trust”, sometimes referred to as a “Qualified Income Trust”. The Trust takes its name from the case of Miller v. Ibarra, 746 F. Supp. 19 (D. Colo. 1990), and is specifically sanctioned by 42 U.S.C. § 1396p(d)(4)(B). The Trust may be used when the countable resources of a Medicaid applicant may be sufficiently low for Medicaid qualification, but the applicant’s monthly income is too high for those states that look to an income limit as a basis for Medicaid qualification. However, the available income is not enough to pay the cost of long-term care in a skilled nursing facility. This Trust is designed to address this problem by bridging the gap between the income cap for eligibility and the actual cost of nursing home care. The Miller trust is significant in those states which impose an income cap on Medicaid long-term care eligibility.

The Miller trust can be named as the recipient of the individual's income, from a pension plan, Social Security, or other source. A portion of the income is expended for the benefit of the applicant (typically paid to a nursing home) with remaining income falling below the Medicaid qualification amount, making the applicant income eligible for Medicaid. The remaining income may be used to satisfy a personal needs allowance of the applicant, a maintenance payment for a community spouse, etc. Upon the death of the beneficiary, the State Medicaid agency must be paid back for its medical assistance from any remaining assets in the Miller trust. If the repayment is accomplished, and assets remain, they may be left to the individual’s heirs. The trust must be irrevocable and the applicant should not be the trustee.

SUGGESTED CLE COURSES: Please note: Mr. Siegel's "Social Security, Medicare And Medicaid: What You Need To Know" is currently available on audio CD and DVD at www.nlfcle.com and online at www.nlfonline.com. On both of these web sites, click on your state (or any state if you do not care about earning CLE credits) and scroll down to the course title which appears under the heading "Other". "Planning For The New Medicare Taxes" appears under the heading "Estate Planning".

Author:

Steven G. Siegel is president of The Siegel Group, which provides consulting services to attorneys, accountants, business owners, family offices and financial planners. Based in Morristown, New Jersey, the Group provides services throughout the United States. Mr. Siegel is the author of many books, including: The Grantor Trust Answer Book (2012 and 2013 CCH); CPA’s Guide to Financial and Estate Planning (AICPA 2012); and Federal Fiduciary Income Taxation (Foxmoor 2012). In conjunction with numerous tax planning lectures he has delivered for the National Law Foundation, Mr. Siegel has prepared extensive lecture materials on the following subjects: Planning for An Aging Population; Business Entities: Start to Finish; Preparing the Audit-Proof Federal Estate Tax Return; Business Acquisitions: Representing Buyers and Sellers in the Sale of a Business; Dynasty Trusts; Planning with Intentionally-Defective Grantor Trusts, Introduction to Estate Planning; Intermediate-Sized Estate Planning; Social Security, Medicare and Medicaid: Explanation and Planning Strategies; Subchapter S Corporations: Using Trusts as Shareholders; Divorce and Separation: Important Tax Planning Issues; The Portability Election; Generation-Skipping Transfer Tax: A Comprehensive Review; and many other titles. Mr. Siegel has delivered hundreds of lectures to thousands of attendees in live venues and via webinars throughout the United States on tax, business and estate planning topics on behalf of numerous organizations, including The Heckerling Institute on Tax Planning, CCH, National Law Foundation, AICPA, Western CPE, the National Society of Accountants, the National Tax Institute, Cohn-Reznick, Professional Education Systems, Inc., Foxmoor Education, many State Accounting Societies and Estate Planning Councils as well as on behalf of private companies. He is presently serving as an adjunct professor of law in the Graduate Tax Program (LLM) of the University of Alabama, and has served as an adjunct professor of law at Seton Hall and Rutgers University law schools. Mr. Siegel holds a bachelor’s degree from Georgetown University (magna cum laude, phi beta kappa), a juris doctor from Harvard Law School and an LLM in taxation from New York University Law School.

-

12 Elder & Family Law Forms (12 Forms, 162 Pages)Special Price $399.00 Regular Price $449.00

12 Elder & Family Law Forms (12 Forms, 162 Pages)Special Price $399.00 Regular Price $449.00

-

12 Elder & Family Law Forms (12 Forms, 162 Pages)Special Price $399.00 Regular Price $449.00